While many of our regular readers are very familiar with the nuances of innovation, it’s such a difficult concept that we still come across a lot of confusion and misinformation surrounding the term in most companies – and of course the population at large.

Especially in light of recent events, innovation is seemingly on everyone’s lips, so we thought it would be important to clarify what it really means.

There’s naturally a good reason for this popularity: innovation is what essentially drives humanity forward, both in terms of well-being, but also economic growth.

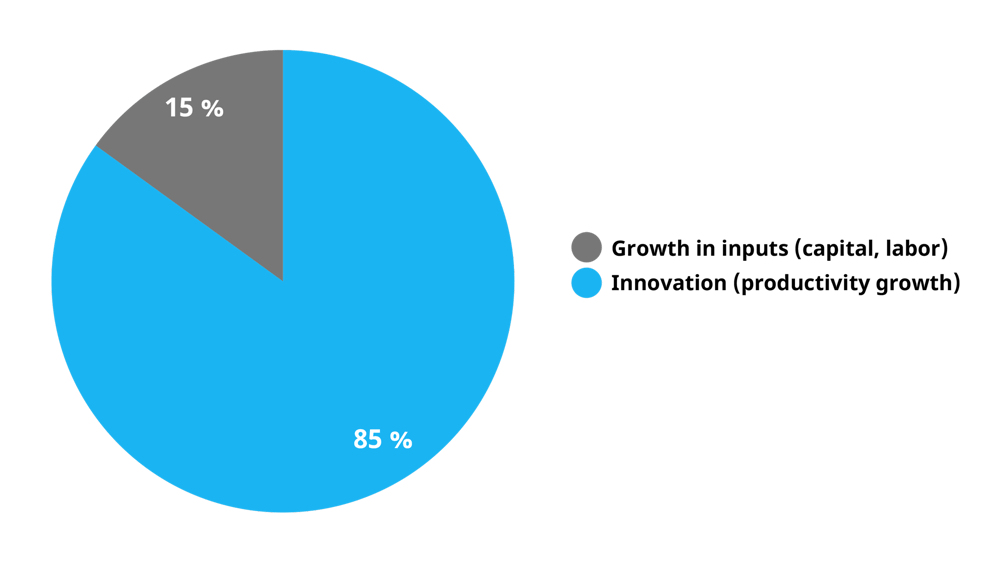

According to OECD research, 85% of all economic growth in the US economy between 1870 and 1950 actually is a result of innovation.

So, even if some of the latest technologies and companies using them are often overhyped, in the long run, innovation is what both companies and investors should really be investing in.

Table of contents

Definition and true meaning of innovation

Let’s start by first defining what the term actually means.

There are literally hundreds, if not thousands, of different definitions for the word “innovation” out there, so just getting to the root of what the term actually means, can be challenging. There just isn’t a clear consensus in the industry on what the correct definition is.

We have gone through the vast majority of these definitions, and for the most part, the differences are actually relatively minor and academic in nature.

In general, everyone agrees that innovations are “novel”. Many argue that it’s not an innovation, but an invention, unless it “creates value”.

The challenge is that these are both naturally very subjective terms.

- Does something have to be “new” or “novel” to the entire world for it to count as an innovation? What about your industry or market? Or just for your company?

- For whom should it “create value”? For customers? For the company and its shareholders? What about the society at large?

- And how do you even define value? Is it just monetary value, or do softer measures count as well? What if it creates tremendous value for some individuals, but is harmful at large?

Thus, it's virtually impossible to come up with a truly objective way to tell if something is an innovation – or not. Thus, it’s probably best to keep the definition of the word quite accommodating.

Our favorite is that by the Merriam-Webster online dictionary:

The introduction of something new.

– Merriam-Webster online dictionary

In other words, innovation is simply anything new that you do.

It can be new products or services, a new manufacturing process that saves a lot of resources, or even just a minor improvement in an existing product or process.

Using the term “innovation” in practice

Knowing how often people interpret the term “innovation” in so wildly different ways, those of us who are in the business of trying to make it happen should obviously be mindful of the challenges that careless use of the term may lead to.

So, whenever you’re talking about “innovation” with a new audience, it’s often helpful to start by ensuring that you’re on the same page when it comes to the terminology, or your conversation might turn out to not be as productive as you hoped it would be. A nice and very practical way to achieve this goal is to actually not use the term “innovation” in the first place. Even though you’d still be going after innovation, it can often be easier to get your message through if you talk about ideas, improvements, changes or new businesses instead, especially if you’re working in a conservative organization.

A nice and very practical way to achieve this goal is to actually not use the term “innovation” in the first place. Even though you’d still be going after innovation, it can often be easier to get your message through if you talk about ideas, improvements, changes or new businesses instead, especially if you’re working in a conservative organization.

What can we learn from the experts – our favorite quotes on innovation

Since innovation is a topic that some of the smartest minds on our planet have put a lot of thought into, we thought it would also make sense to provide you with a few of our favorite quotes on innovation. They really do a great job of capturing the essence of innovation.

“Innovation is taking two things that exist and putting them together in a new way.“

Tom Freston (born 1945), Co-founder of MTV

“What is the calculus of innovation? The calculus of innovation is really quite simple: Knowledge drives innovation, innovation drives productivity, productivity drives economic growth.“

William Brody (born 1944), Scientist

“Creativity is thinking up new things. Innovation is doing new things.“

Theodore Levitt (1925 – 2006), Renown economist

“You can’t wait for inspiration, you have to go after it with a club.“

Albert Einstein (1879 – 1955), Mathematician

“I have not failed. I’ve just found 10,000 ways that won’t work.“

Thomas Edison (1847 – 1931), Inventor

“There’s a way to do it better. Find it.“

Thomas Edison (1847 - 1931), Inventor

“The riskiest thing we can do is just maintain the status quo.“

Bob Iger (born 1951), Media executive & businessman

“When the winds of change blow, some people build walls and others build windmills.“

An ancient Chinese proverb

“Innovation- any new idea- by definition will not be accepted at first. It takes repeated attempts, endless demonstrations, monotonous rehearsals before innovation can be accepted and internalized by an organization. This requires courageous patience.“

Warren Bennis (1925 – 2014), Scholar and organizational consultant

Lessons learned

When we put all of those thoughts together, what can we learn?

- Innovation is ultimately about putting the figurative 1 + 1 of existing knowledge together to create something novel.

- Innovation takes a lot of hard work, it’s not just about being creative or coming up with a great idea.

- Innovation always feel risky and new ideas will usually be resisted, that’s just a part of the process.

- Still, the riskiest thing you can do is to try to stick with the past and not embrace the change.

Common misconceptions about innovation

Now that we’ve understand the big picture, let’s clear a few of the most common misconceptions about innovation.

“Innovation is something startups do”

This is probably one of the most common misconceptions out there.

Sure, many startups are tremendously innovative, and drive a significant portion of the innovation in our society, but that

-

- doesn’t mean that all startups would be innovative

- doesn’t mean that large organizations wouldn’t innovate

First of all, not every startup is innovative. If you decide to open up a lemonade stand and set up a company for it, it is a startup, but there probably isn’t anything new or innovative there. Second, large organizations (companies, universities, and research institutes included) actually create a big portion of innovations out there.

Second, large organizations (companies, universities, and research institutes included) actually create a big portion of innovations out there.

Just think of the device you’re using to read this article. It’s without a doubt a product created and sold by a large company, with most of the meaningful hardware and software components on it also being developed by other large organizations.

It’s actually the medium-sized organizations that are usually worst positioned to innovate: they don’t have the resources of the big companies, and unlike startups, they usually have existing processes in place, as well as something to lose, which makes them less likely to want to embrace change and innovation.

This is something we very much empathize with, and it’s a big part of our mission to help them change this.

“Build and they will come”

This is the traditional way people approached innovation. You simply created a pretty good product, and usually people came and found you.

Well, these days, most of us in the developed world have most of our basic needs met, and there’s so much information and so many different products and services out there, that it doesn’t usually work like that anymore.

These days, you have to start by truly, deeply, understanding your customer, and the specific problems they’re trying to solve, or you’re very likely to fail at innovation.

“Innovation has to be a groundbreaking technological invention”

Many still think that innovations have to be these big, disruptive, groundbreaking inventions.

Well, as we covered earlier, that simply isn’t true. Usually even the groundbreaking discoveries and inventions need many additional, smaller improvements and innovations to actually become commercially feasible. Just think of something like electric cars: it was first invented more than 100 years ago and is just now on the verge of becoming mainstream.

Usually even the groundbreaking discoveries and inventions need many additional, smaller improvements and innovations to actually become commercially feasible. Just think of something like electric cars: it was first invented more than 100 years ago and is just now on the verge of becoming mainstream.

In addition, innovations can be any kind of novel, even seemingly minor things, that just make a difference in the grand scheme of things. They don’t even have to be technological at all.

As a matter of fact, marketing and business model innovations are incredibly powerful forms of innovation, that don’t require you to necessarily invest in cutting edge research.

Even a few relatively simple improvements in some of your internal processes can be the difference between being profitable or not, so incremental innovations are usually very important, especially for large companies.

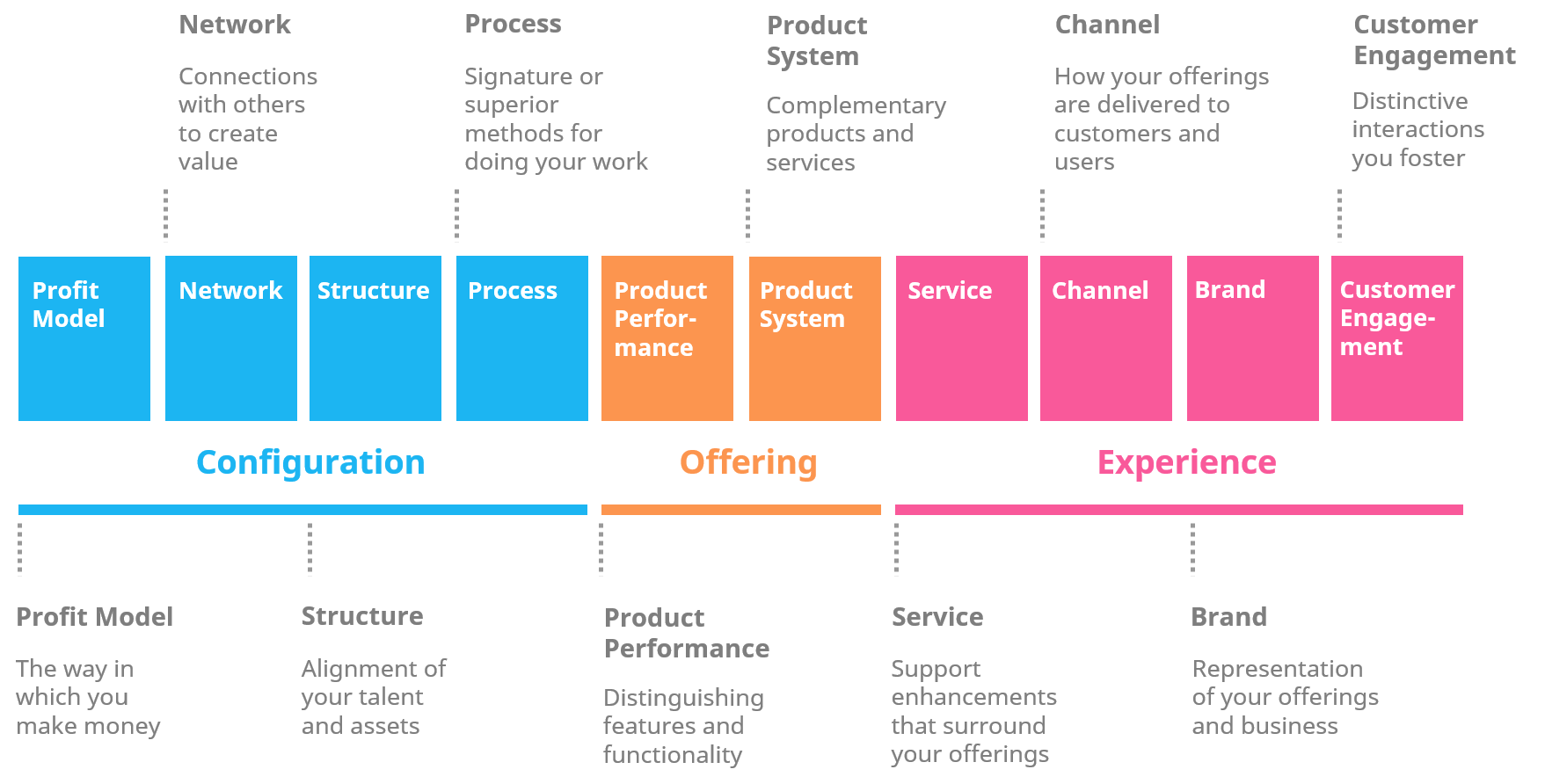

A great way to understand how diverse innovation really can be, is the ten types of innovation framework, depicted below.

Examples of successful innovations

So, what do successful innovations then look like?

Well, everyone is familiar with those big new technological breakthroughs that changed the world, like the lightbulb, and the Internet, so we’ll next show a few more subtle examples of successful innovations from throughout history.

The subscription business model

Business model innovation is one of the most powerful, yet simultaneously underappreciated forms of innovation.

While the business model itself is obviously pretty old, it’s been successfully used for ages in things like newspapers and season tickets, it’s really gained incredible popularity in the last couple of decades.

After Salesforce pioneered the Software as a Service business model in the early 2000s, we’ve literally seen an explosion in subscription businesses, and for good reason.

A subscription business model makes it easier for customers to buy as they aren’t forced to make an upfront investment and have the flexibility to end their subscription whenever they want. For the business, it aligns their interests with the customer, provides a more predictable source of revenue, and ultimately allows them to increase profitability down the road.

It’s a great example of a seemingly simple change that can make all the difference between success and failure.

Seasonal crop rotation

Way back in the day when humans first started cultivating crops, a similar pattern emerged in many diverse geographical areas.

Thanks to the agricultural revolution, population quickly began to grow. As the population grew, more and more land was needed to grow food for everyone. Farmland thus expanded until there was no more arable land in the vicinity to expand to.

At that point, people often started cultivating the land more aggressively and only chose to plant the most productive crops to cope with the increased demand. Unfortunately, that only made things worse.

Unfortunately, that only made things worse.

When you plant the same crop in the same place year after year, the soil will gradually lose more and more of its nutrients. This will in turn lower crop yields and eventually lead to the land becoming unusable for farming for extended periods of time.

The solution to this problem is incredibly simple: you essentially just rotate the placing of the crops every season and perhaps give the soil a season to rest every now and then.

This seemingly simple process innovation alone was usually enough to preserve the quality of the land and save the lives of thousands, perhaps even millions, of people back when we didn’t have all the fancy technology and knowledge we today possess.

The Ritz-Carlton $2,000 rule

The $2,000 rule is an example of a very different kind of a process innovation, one that focuses on the customer experience.

As a luxury hotel chain, Ritz-Carlton is one of the embodiments of great customer service, and for them to stay in business, they do need to live up to their reputation.

To ensure that is the case, they’ve long had the so called $2,000 rule, which as the name would suggest, indicates that any frontline employee can spend up to $2,000 right away without asking their manager for permission to address any and all problems customers might face.

And that is not $2,000 per year, but $2,000 per incident. This might raise a few eyebrows at first, but when you consider that their customers spend an average of $250,000 during their lifetime, it suddenly makes a lot of sense. By having such a rule in place, employees tangibly know how highly the management not only values the customer experience, but also trusts their judgment. As a result, they behave accordingly, which in turn leads to a far superior experience than your average run of the mill hotel.

By having such a rule in place, employees tangibly know how highly the management not only values the customer experience, but also trusts their judgment. As a result, they behave accordingly, which in turn leads to a far superior experience than your average run of the mill hotel.

The same exact rule might not make sense for your business, but it’s still a great example of a really simple change that can make a huge difference in making customers lives’ much easier.

How does innovation happen in practice?

So, now that you have a pretty good of what innovations really is, the question remains, how do you actually create one?

Well, it’s a whole art and a science of its own, there isn’t necessarily just one “right way to innovate”.

What’s more, the answer also depends highly on whether you’re looking to create smaller, incremental innovations, or perhaps the bigger, more outside the box, breakthrough innovations.

Also, if you’re looking to innovate as a startup, the challenges you face will be somewhat different than if you were to innovate within a large incumbent organization.

However, there are also many similarities. Here’s the high-level overview of the way we like to approach this:

-

- Identify a meaningful problem, if it’s a big one, break it down into smaller chunks

- Find the best solution with first principles thinking

- Solve the problem(s) and create real value

- Keep an open mind and continuously look for things to improve upon

That's of course easier said than done. Still, it's important to keep the big picture in mind and not get lost in the weeds.

In essence, you should usually start by identifying a meaningful problem you’d like to solve for your customers. Alternatively, this could also be a bigger, more far flung but ambitious and concrete objective.

Almost never can you solve these meaningful problems with just a single innovation, so what you then need to do is to break the problem or objective into smaller chunks.

Then, you can simply start solving the problem or problems, one by one. Just make sure to do it in a way that creates real, tangible value.

The above two steps are essentially what all agile methods and movements like the lean startup are all about.

Finally, to get to the best possible solution, you should keep an open mind and continuously look for better ways to solve the problem and achieve your objectives, and the way you do that is by embracing first principles thinking.

Conclusion

If innovation is an art and a science of its own, so is the act of making it happen in organizations. This is what’s referred to as innovation management, or the ability to systematically introduce new things and manage the whole process in a way that helps you make innovation more predictable and scalable.

It’s such a big topic, and one that we’ve written about quite extensively, that we won’t cover it in more detail here. However, if you are looking to make more innovation happen in your organization, a great place to start from is our Innovation System Online Coaching Program. It is an online program that will walk you through the process of making more innovation happen in your organization, step-by-step.

And, if you'd like to receive the latest insights on innovation, leadership, and culture to your inbox once a month, please consider subscribing.